TrustQ Analysis

The Middle East War and Trust in the Energy Sector

May 5, 2026

Beyond Oil Prices:

The Trust Breakdown Behind the Middle East Energy Crisis

C-Suite Presentation to Major Energy Company

Advisory Note: This analysis is for informational purposes only

and does not constitute investment, legal, or tax advice.

Please see the full Legal Disclaimer at the end of this article.

Optimal Trust Grid Snapshot:

Public Trust in the Energy Sector During the Middle East War

Scoring intent: These scores measure current trust conditions in the system. They are not moral judgments.

Rational Trust = evidence-based predictability.

Emotional Trust = perceived safety, fairness, legitimacy, and human alignment.

The war in the Middle East has become more than a military conflict. It has become a live stress test of the global energy system.

The immediate question is obvious: Can the world keep energy flowing?

The deeper question is more dangerous: Do people still trust the energy sector when the system is under pressure?

That question is exactly right. The crisis is not merely moving oil prices. It is altering the public’s perception of energy companies, governments, exporters, regulators, shipping lanes, and the entire architecture by which modern civilization is powered.

This is not just an energy-price story. It is a trust-in-essential-infrastructure story.

Energy is one of the few sectors that people experience both materially and emotionally. When energy works, it disappears into the background. When it fails, it becomes personal: the gas pump, the heating bill, the airline ticket, the grocery price, the job risk, the national-security anxiety. In a war-driven energy shock, the public does not merely ask whether energy companies are competent. It asks whether they are fair, honest, aligned, and worthy of the power they hold.

Advisory Note

This analysis is for informational and educational purposes only. It does not constitute investment, legal, tax, geopolitical, or energy-trading advice.

TRUSTQ Newsfeed — May 5, 2026

Middle East War: Hormuz disruption, oil shock, and a trust test for the global energy system

What happened: ground truth from major reporting

The United States and Israel launched joint air strikes on Iran on February 28, 2026, triggering sharp disruption across Middle Eastern energy flows and sending Brent crude close to $120 per barrel before partial easing. (IEA)

The Strait of Hormuz remains the central pressure point. The International Energy Agency reports that crude and oil-product flows through the Strait fell from roughly 20 million barrels per day before the war to just over 2 million barrels per day in March. Alternative export routes increased, but not enough to compensate for the scale of the disruption. (IEA)

The IEA’s April 2026 Oil Market Report identifies the resumption of flows through Hormuz as the “single most important variable” for easing pressure on energy supplies, prices, and the global economy. (IEA)

Reuters reported on May 5 that oil prices dropped about 3% after a U.S.-flagged vessel passed through the Strait of Hormuz under U.S. military escort, but Brent remained around $110.61 and WTI around $102.19. (Reuters)

The AP reports that a proposed U.N. resolution, backed by the United States and Gulf nations, threatens Iran with sanctions or other measures unless it stops attacks on ships, stops collecting alleged illegal tolls, and discloses mine placements in the Strait. (AP News)

Goldman Sachs warned that global oil stocks are approaching an eight-year low, with refined product buffers also falling sharply since the onset of the conflict. (Reuters)

This is not merely a war story. It is a system-confidence story. The world is watching whether the energy system can keep functioning when its most strategic artery is threatened.

Core TrustQ Thesis

The Middle East war is affecting trust in the energy sector by forcing the public to confront a brutal paradox:

Energy companies are most needed when the public is most vulnerable — but they are also most mistrusted when prices rise, supplies tighten, and profits appear to benefit from crisis.

That is the heart of the trust rupture.

The sector may be operationally necessary. But necessity is not the same as trust.

The public may depend on oil, gas, LNG, shipping, refining, utilities, and energy infrastructure. But dependence can deepen resentment if people believe the system is opaque, opportunistic, politically protected, or insufficiently aligned with ordinary citizens.

In Optimal Trust terms, the war is degrading trust across all six trust components:

- Aligned Interests — Are energy companies seen as aligned with consumers, or with profits and geopolitics?

- Competency — Can the sector keep supply flowing under extreme stress?

- Communications — Is the sector explaining the crisis clearly, or hiding behind market complexity?

- Shared Values — Does the sector stand for public resilience, or merely extraction and returns?

- Intentions — Are companies stabilizers, beneficiaries, or silent opportunists?

- Integrity — Are pricing, profits, exports, and public claims perceived as fair and legitimate?

The conflict is therefore not only testing physical supply. It is testing the moral and emotional legitimacy of the energy sector.

The Optimal Trust Grid:

Bottom-Line Grid Reading

The energy sector is not experiencing a total trust collapse. It is experiencing something more subtle and more dangerous:

Functional dependence with emotional mistrust.

People still need the sector. Governments still rely on it. Markets still price it. Militaries still protect it. Economies still run through it.

But emotional trust is deteriorating because the public sees a system that appears indispensable, expensive, opaque, and structurally advantaged during crisis.

That combination is volatile.

Why These Scores Are Where They Are

The OT Diagnosis

- Competency is the strongest component — but only at the operational level

The energy sector still receives partial rational credit for competence. Oil, LNG, refining, shipping, and trading systems are adapting. Alternative routes from Saudi Arabia’s west coast and Fujairah have increased, even though they cannot fully replace Hormuz volumes. (IEA)

But the public does not experience that as competence. The public experiences the result: higher prices, uncertainty, and fear of scarcity.

So the sector’s Group Rational Competency is mildly positive, while Individual Emotional Competency remains negative.

The sector may be doing difficult work under extraordinary conditions. But if consumers still feel exposed, anxious, and uninformed, operational competence does not translate into public trust.

- Communications are weak because the story is too complex and too fragmented

The public is hearing too many signals at once: military escort operations, Iranian threats, U.N. resolutions, oil-price swings, LNG exposure, inflation warnings, and company statements about supply discipline. The AP’s reporting on a proposed U.N. resolution shows how the crisis is now simultaneously military, diplomatic, maritime, humanitarian, and economic. (AP News)

That complexity creates a communications vacuum.

Energy companies often explain crises in market language: supply disruption, spare capacity, route optionality, risk premium, refinery slates, contractual obligations. Those terms may be accurate. But they do not answer the public’s emotional question:

Are you looking out for us?

When that question is not answered, mistrust fills the silence.

- Aligned Interests are the central fracture

The public understands that energy companies must operate profitably. But during a war shock, profitability becomes morally charged.

If oil prices rise, energy companies may be seen as benefiting from geopolitical pain. If U.S. exports increase while domestic fuel prices remain high, the public may ask whether the industry is serving national consumers or global price opportunities. If supply remains tight, consumers may suspect that scarcity is being managed for advantage.

That does not mean the suspicion is always factually correct. But TrustQ does not measure only facts. It measures the relationship between facts and perception.

The aligned-interests problem is therefore severe:

The sector’s actual function is stabilization. Its perceived function may become extraction.

- Integrity is under pressure because price fairness is emotionally judged

In energy crises, people rarely understand the mechanics of global pricing. They understand the bill.

That bill becomes a moral document.

When gasoline, diesel, heating, utility, and transportation costs rise, consumers infer intent from price. If companies report strong profits while households suffer, public trust erodes even if the profits are explainable through global market dynamics.

Integrity is therefore not only about legal compliance. It is about whether the system feels legitimate.

Right now, the sector’s integrity problem is this:

People may believe the market is functioning exactly as designed — and still believe the design is unfair.

- Shared Values are weak because the energy transition narrative is fracturing

Before the war, much of the public debate centered on climate, renewables, fossil fuels, and transition speed. The war has scrambled that debate.

For some, the crisis proves the need for more domestic fossil-fuel production. For others, it proves the danger of continued dependence on oil and gas chokepoints. For others, it strengthens the case for nuclear, renewables, storage, distributed generation, and energy independence.

The sector is therefore not facing one public. It is facing multiple publics with incompatible values.

The war does not settle the energy-transition argument. It intensifies it.

- Intentions are opaque

Energy companies may see themselves as providing continuity under stress. Governments may see them as strategic infrastructure. Investors may see them as risk-adjusted capital allocators.

But many citizens may see something else: a sector that speaks cautiously, benefits from price spikes, resists political blame, and avoids moral clarity.

That is an intentions problem.

In trust terms, silence is not neutral. During crisis, silence is interpreted.

Market Meaning in Two Time Horizons

- Immediate reaction: days to weeks

“Risk repricing plus emotional volatility”

The near-term market is trading around one dominant variable: whether Hormuz flows normalize or deteriorate further. The IEA identifies resuming flows through the Strait as the central variable for easing energy pressure, while Reuters reports that even positive shipping developments are being treated cautiously by analysts. (IEA)

Immediate effects:

- Oil prices remain volatile.

- Refined product buffers are tightening.

- Shipping risk and insurance risk remain elevated.

- LNG exposure is acute, especially for countries dependent on Gulf exports.

- Governments face rising subsidy, inflation, and consumer-protection pressure.

- Energy companies face the reputational risk of being seen as crisis beneficiaries.

TrustQ interpretation:

The market is pricing barrels. The public is pricing fairness.

That is why energy-company communications cannot focus only on supply. They must address legitimacy.

- Medium term: months to years

“Resilience, transition credibility, and institutional trust”

If the war drags on, the energy sector’s trust challenge will shift from crisis management to systemic legitimacy.

The question will become:

Did the energy sector help society become more resilient — or did it simply pass through costs and protect its own position?

That medium-term question will affect:

- Public tolerance for fossil-fuel investment.

- Political support for domestic production.

- Acceleration or delay of energy-transition policy.

- Trust in LNG and global supply chains.

- Trust in energy companies’ climate commitments.

- Trust in pricing, profits, and exports.

- Trust in governments that rely on private energy companies during crisis.

This is where the war becomes a reputational inflection point.

What Energy Leaders Should Say

Scripts That Work

The core framing

“This is not only an oil-price shock. It is a resilience test for the global energy system. Our responsibility is to help maintain supply, explain constraints honestly, avoid false certainty, and show that we understand the pressure households, businesses, and governments are facing.”

Why it works: It acknowledges both rational and emotional trust. It does not hide behind technical language. It states responsibility without pretending to control everything.

If asked: “Are energy companies profiting from war?”

“Higher prices can improve financial results for parts of the sector, and we should be direct about that. But the central issue is not whether prices move. The central issue is whether companies act responsibly when they do. That means supply discipline, transparent communication, support for customers where possible, and visible commitment to system stability.”

Why it works: It does not deny the obvious. It shifts the trust test from optics to conduct.

If asked: “Does this prove we need more fossil fuels?”

“It proves we need a more resilient energy system. That includes reliable conventional supply, diversified routes, LNG security, grid resilience, storage, nuclear, renewables, and demand flexibility. The lesson is not one fuel versus another. The lesson is that energy systems fail when they are too concentrated, too opaque, or too brittle.”

Why it works: It avoids ideological capture and frames the issue through resilience.

If asked: “Why should the public trust the energy sector?”

“The public should not be asked for blind trust. Trust has to be earned through performance, transparency, fairness, and accountability. In a crisis like this, the sector has to show not only that it can deliver energy, but that it understands the human consequences of disruption.”

Why it works: It refuses defensive corporate posture. It raises the standard.

TrustQ Playbook

What energy companies should do now

- Map trust exposure, not only supply exposure

Companies should map the stakeholders whose trust is now under pressure:

- Consumers and households.

- Commercial and industrial customers.

- Governments and regulators.

- Investors.

- Employees.

- Communities.

- Import-dependent countries.

- Climate-transition advocates.

- National-security stakeholders.

- Media and civil-society observers.

The key question is not simply “Who is affected?” It is:

Who now believes the energy system is failing them?

- Separate operational facts from moral perception

A technically correct explanation may still fail emotionally.

For example:

- “Prices are set globally” is true.

- “Supply chains are constrained” is true.

- “We do not control geopolitical events” is true.

But none of those statements answers the emotional trust question:

Are you acting with fairness under pressure?

Energy-sector communications must therefore operate on two channels:

- Rational channel: supply, routes, capacity, production, reserves, constraints.

- Emotional channel: fairness, burden-sharing, responsibility, empathy, transparency.

- Pre-commit to crisis conduct principles

The sector should articulate visible principles:

- No misleading price explanations.

- No exaggerated claims of control.

- No triumphalist profit messaging.

- Transparent explanation of exports and domestic impacts.

- Clear distinction between market price effects and company decisions.

- Support for vulnerable customers where applicable.

- Public cooperation with governments on resilience.

- Continued credibility on long-term transition.

This is not public relations cosmetics. It is trust governance.

- Use the crisis to define resilience, not ideology

Energy companies should not frame the war as a simple vindication of fossil fuels. That will deepen mistrust among climate-sensitive stakeholders.

Nor should transition advocates pretend current fossil-fuel dependency can disappear overnight. That damages competency trust.

The more credible frame is:

The future energy system must be secure, affordable, lower-carbon, diversified, and resilient under geopolitical stress.

That is the common-ground message.

Sector Impact Add-On

How the war affects trust in the energy sector

- Integrated oil and gas companies

Immediate

Integrated majors may receive rational credit for scale, logistics, expertise, and ability to maintain supply under stress. But they also face emotional mistrust if the public sees them as gaining from war-driven scarcity.

OT drivers:

Competency up modestly; Aligned Interests, Intentions, and Integrity under pressure.

Medium term

The reputational question becomes whether integrated energy companies can credibly position themselves as resilience institutions rather than profit-maximizing commodity actors.

Trust risk:

“Essential but mistrusted.”

Trust opportunity:

“Stabilizer of civilization under stress.”

LNG exporters and import-dependent economies

Hormuz disruption has direct LNG implications because Gulf LNG flows are difficult to reroute. The IEA notes that the Strait is a primary export route for oil produced across the Gulf and that prolonged disruption could render much of the world’s spare production capacity unavailable. (IEA)

Immediate

LNG buyers, especially in Asia, will worry about physical availability, price spikes, and contract reliability.

Medium term

Trust in LNG as a transition fuel may be damaged if buyers conclude that LNG is too geopolitically concentrated.

OT drivers:

Competency, Integrity, and Aligned Interests.

- Refining, shipping, and trade finance

When the crisis hits shipping lanes, the energy story becomes a logistics story.

Insurance, maritime security, letters of credit, sanctions compliance, port access, and cargo title all become trust variables.

Immediate

War-risk premiums rise. Shipping decisions become politicized. Buyers wonder whether contracted supply can actually arrive.

Medium term

Companies that communicate clearly about logistics constraints gain trust. Companies that obscure risk lose trust.

OT drivers:

Communications and Integrity.

- Utilities and downstream consumer-facing energy

Utilities and downstream providers may not cause the shock, but they become the face of the shock.

Consumers do not experience the Strait of Hormuz. They experience bills.

Immediate

Public anger may be directed at the most visible local energy provider, even if the root cause is global.

Medium term

Customer-trust strategies become essential: bill transparency, hardship programs, conservation guidance, and honest explanation of pass-through costs.

OT drivers:

Communications, Aligned Interests, Emotional Integrity.

- Renewables, nuclear, and storage

The war creates a trust opening for non-fossil energy, but only if the message is disciplined.

A simplistic “this proves fossil fuels are bad” message may feel opportunistic. A more credible message is:

Energy security now requires diversified systems that reduce exposure to geopolitical chokepoints.

Immediate

Renewables and nuclear gain strategic relevance.

Medium term

The energy-transition debate shifts from climate-only to resilience-plus-climate.

OT drivers:

Shared Values, Competency, Meta-Group Aligned Interests.

Impact on 3 Market Proxies

Scenario ranges, not forecasts

These are scenario frames for disciplined discussion, not trading recommendations.

Proxy 1 — Brent / WTI crude

Base case: 50%

“Fragile partial reopening”

- Brent / WTI: volatile, broadly rangebound at elevated levels.

- Drivers: limited Hormuz flows, military escort operations, uncertainty over ceasefire durability.

- OT trigger: Group Competency remains strained; Meta-Group Integrity remains negative.

Reuters reported oil falling about 3% after a successful escorted vessel passage, but prices remained elevated and analysts warned against treating the event as full normalization. (Reuters)

Stress case: 30%

“Renewed attacks or wider closure”

- Brent / WTI: sharp upside risk.

- Drivers: new attacks, mines, insurance withdrawal, retaliation, shipping freeze.

- OT trigger: Integrity and Competency deteriorate at the global-system level.

Relief case: 20%

“Credible reopening and enforceable maritime security”

- Brent / WTI: risk premium fades.

- Drivers: multilateral guarantees, reduced attacks, reliable vessel passage.

- OT trigger: Communications and Competency improve.

Proxy 2 — Energy equities

Base case: 50%

“Higher price support, higher scrutiny”

- Energy equities may benefit from elevated prices.

- But reputational and political scrutiny increases.

- Companies with strong balance sheets and diversified operations likely fare better than highly exposed or politically vulnerable names.

Bull case: 25%

“Sustained price premium plus capital discipline”

- Strong cash flow.

- Investor support for disciplined producers.

- Sector viewed as strategically indispensable.

Bear case: 25%

“Political backlash against perceived profiteering”

- Windfall-tax rhetoric, export scrutiny, price-control pressure.

- Trust damage offsets commodity upside.

- Emotional trust deterioration becomes policy risk.

Proxy 3 — Inflation-sensitive consumer sectors

Base case: 55%

“Margin pressure and consumer anxiety”

- Airlines, transportation, retail, chemicals, and manufacturing face cost pressure.

- Consumers blame visible price channels.

- Energy becomes a household political issue again.

Stress case: 25%

“Energy inflation feeds broader economic mistrust”

- Food, fertilizer, logistics, and transport costs rise.

- Trust in both government and energy companies deteriorates.

Relief case: 20%

“Supply confidence stabilizes inflation expectations”

- Prices remain high but less chaotic.

- Public anger recedes if communications improve and volatility declines.

The Most Important OT Lever to Watch

If you track only one thing, track:

Aligned Interests + Integrity at the Individual Emotional level

That is where the energy sector is most exposed.

The public will ask:

- Are companies sharing pain or exploiting it?

- Are explanations honest or evasive?

- Are exports, profits, and prices being handled fairly?

- Are consumers protected or merely managed?

- Are companies acting like public infrastructure or private fortresses?

This is the trust-cell cluster that will determine whether the energy sector comes out of the crisis seen as a stabilizing force or a profiteering class.

Bottom-Line Trust Diagnosis

Primary rupture

Aligned Interests + Integrity

The public may believe the sector is necessary but not sufficiently aligned with ordinary people.

Primary market transmission

Hormuz disruption → energy-price volatility → inflation pressure → public anger → political scrutiny → sector-trust deterioration

Trust posture

- Rational trust: damaged but not collapsed. The sector still has operational credibility.

- Emotional trust: significantly impaired. The sector risks being seen as benefiting from pain.

- Strategic trust: unstable. The public is reconsidering what kind of energy system is truly secure.

Final diagnosis

This crisis does not destroy trust in the energy sector. It reveals the condition of that trust.

And what it reveals is uncomfortable:

The world trusts energy to function. It does not yet trust energy to be fair.

Appendix 1

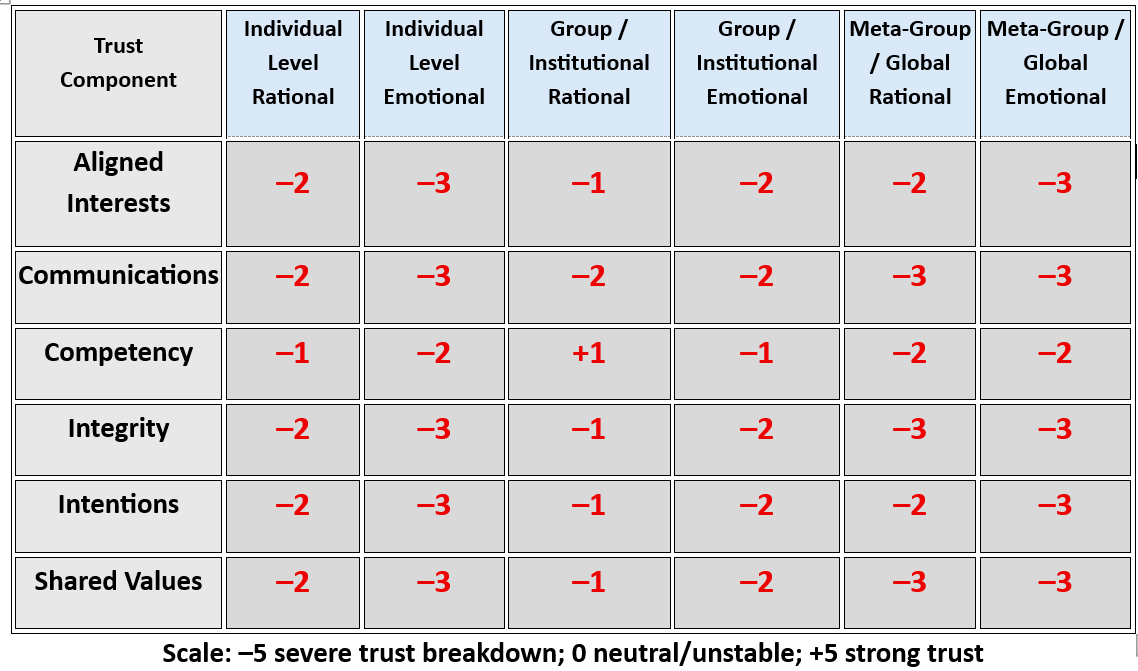

Detailed Optimal Trust Grid Scoring

Aligned Interests

Individual Level

Rational: –2

Consumers know they need energy companies, but they do not believe company incentives are fully aligned with household affordability.

Emotional: –3

Rising prices during war create resentment. The public may feel trapped inside a system that profits when people suffer.

Group / Institutional Level

Rational: –1

Governments, companies, shippers, refiners, and importers share an interest in keeping energy flowing. But their incentives diverge around price, exports, national priorities, and political blame.

Emotional: –2

Institutional trust is strained by suspicion: consumers suspect companies; companies fear political intervention; governments fear public backlash.

Meta-Group / Global Level

Rational: –2

The world shares an interest in open energy corridors, but national interests diverge sharply.

Emotional: –3

Import-dependent countries may feel abandoned or exploited by a global system they cannot control.

Communications

Individual Level

Rational: –2

Consumers receive fragmented explanations about global prices, war risk, refining capacity, and shipping constraints.

Emotional: –3

The language of markets does not satisfy the emotional need for reassurance and fairness.

Group / Institutional Level

Rational: –2

Companies, governments, traders, and international bodies are not speaking from a single narrative.

Emotional: –2

The absence of unified explanation creates anxiety and distrust.

Meta-Group / Global Level

Rational: –3

The international system lacks clear, shared messaging on Hormuz security, sanctions, maritime rules, and supply normalization.

Emotional: –3

Global publics see confusion, escalation, and partial information.

Competency

Individual Level

Rational: –1

Consumers see the system still functioning, but at higher cost and with visible fragility.

Emotional: –2

People feel exposed. Competence does not feel real when bills rise and uncertainty spreads.

Group / Institutional Level

Rational: +1

The sector shows real operational ability: rerouting, inventory management, military coordination, alternative exports, and market adjustment.

Emotional: –1

Despite competence, institutions do not inspire confidence because the disruption remains severe.

Meta-Group / Global Level

Rational: –2

The global energy system has proven too concentrated around critical chokepoints.

Emotional: –2

The public sees fragility in what was supposed to be a modern, managed system.

Integrity

Individual Level

Rational: –2

Consumers question whether prices, exports, and profits reflect unavoidable market forces or opportunistic behavior.

Emotional: –3

Price spikes feel unfair, especially if companies appear calm or profitable while households are under stress.

Group / Institutional Level

Rational: –1

Companies may be acting within lawful market structures, but legality alone does not resolve perceived fairness.

Emotional: –2

Public suspicion increases when corporate explanations feel defensive or technical.

Meta-Group / Global Level

Rational: –3

The rules governing maritime security, sanctions, retaliation, and energy access are under severe strain.

Emotional: –3

The global energy order feels unequal: powerful states protect flows; vulnerable populations absorb costs.

Intentions

Individual Level

Rational: –2

Consumers cannot easily distinguish between companies trying to stabilize supply and companies benefiting from scarcity.

Emotional: –3

Many will emotionally infer bad intent from high prices.

Group / Institutional Level

Rational: –1

Energy companies, governments, and regulators have mixed intentions: stabilization, profit, security, political control, inflation management.

Emotional: –2

Stakeholders suspect hidden agendas.

Meta-Group / Global Level

Rational: –2

Global actors claim to want stability, but the military and diplomatic environment signals conflicting objectives.

Emotional: –3

The public doubts whether the system is organized around human welfare or power.

Shared Values

Individual Level

Rational: –2

Consumers and companies do share a value in reliable energy, but differ sharply on affordability, climate, profits, and responsibility.

Emotional: –3

The crisis deepens the sense that companies and ordinary people live in different moral economies.

Group / Institutional Level

Rational: –1

There is partial overlap around security, reliability, and resilience.

Emotional: –2

Climate advocates, fossil-fuel defenders, national-security voices, and consumer advocates interpret the crisis through competing value systems.

Meta-Group / Global Level

Rational: –3

The world lacks a shared energy compact that balances security, affordability, climate, sovereignty, and fairness.

Emotional: –3

The crisis feels like proof that the global energy system is not morally coherent.

Appendix 2

Trust Repair Levers: What Would Actually Change the Energy-Sector Narrative

The trust breakdown is not irreversible. But it cannot be repaired by advertising.

The sector needs visible conduct that changes what stakeholders believe.

Trust Repair Lever #1

Reframe the sector as a resilience partner, not a crisis beneficiary

What must change

Energy companies should make clear that their role is to stabilize supply, reduce volatility where possible, support customers, and invest in resilience.

This requires plain language:

- What the company controls.

- What it does not control.

- What it is doing to protect supply.

- What it is doing to reduce consumer harm.

- How it is handling profits, exports, and reinvestment responsibly.

OT cells this repairs

- Aligned Interests — Individual Emotional ↑

- Intentions — Individual Emotional ↑

- Integrity — Group Emotional ↑

- Communications — Individual Rational ↑

Market and public signal to watch

- Reduced political rhetoric around profiteering.

- Greater public understanding of supply constraints.

- Less hostile media framing of energy-company earnings.

- Stronger credibility in CEO and CCO messaging.

Translation

“The sector must show that it is not merely earning through volatility. It is helping society withstand volatility.”

Trust Repair Lever #2

Make pricing and exports explainable

What must change

Energy companies and industry groups should explain price formation, export dynamics, refining constraints, and supply obligations in language ordinary citizens can understand.

Not propaganda. Not lobbying language. Explanation.

The public needs to understand:

- Why domestic prices rise when the disruption is overseas.

- Why exports may continue during domestic price pressure.

- What refining constraints matter.

- What companies can and cannot legally or operationally change.

- How profits are being used.

OT cells this repairs

- Communications — Individual Rational ↑

- Integrity — Individual Rational ↑

- Aligned Interests — Individual Emotional ↑

- Competency — Group Rational ↑

Market and public signal to watch

- Fewer accusations of unexplained profiteering.

- Better media literacy around global pricing.

- Less regulatory panic.

- More nuanced investor and consumer response.

Translation

“Complexity is not an excuse. In a trust crisis, complexity must be translated.”

Trust Repair Lever #3

Build the energy-resilience bridge between fossil fuels, renewables, LNG, nuclear, and storage

What must change

The sector must avoid using the war as a narrow ideological weapon.

The credible message is not:

- “This proves fossil fuels are right.”

- “This proves fossil fuels are wrong.”

The credible message is:

“This proves that energy resilience must be diversified, secure, affordable, lower-carbon, and less exposed to geopolitical chokepoints.”

OT cells this repairs

- Shared Values — Meta-Group Rational ↑

- Shared Values — Meta-Group Emotional ↑

- Aligned Interests — Group Rational ↑

- Intentions — Meta-Group Emotional ↑

Market and public signal to watch

- More bipartisan language around resilience.

- Stronger support for infrastructure investment.

- Less polarized energy-transition debate.

- Greater credibility for companies that hold both security and transition in view.

Translation

“The sector earns trust when it refuses false choices.”

Bottom-Line Synthesis

The Middle East war is now a defining trust event for the energy sector.

It tests whether the sector can be seen as:

- Competent enough to keep energy flowing.

- Honest enough to explain what is happening.

- Fair enough not to appear exploitative.

- Aligned enough to care about consumers.

- Responsible enough to support resilience.

- Visionary enough to help build a less brittle system.

The danger is not that the public stops needing the energy sector.

The danger is that the public needs it, depends on it, pays more for it, and resents it all at once.

That is the volatile trust condition.

The central TrustQ conclusion is therefore:

The Middle East war is transforming energy-sector trust from a background assumption into a front-stage test of legitimacy.

Energy companies that communicate only as market actors will lose emotional trust.

Energy companies that communicate as resilience institutions — candid, competent, fair, and visibly aligned with public need — can strengthen trust even in the middle of crisis.

The strategic opportunity is real.

But so is the warning:

In a crisis, the public does not judge the energy sector only by whether it delivers energy. It judges the sector by whether it appears worthy of the power civilization has given it.

Legal Disclaimer

This TrustQ Newsfeed content is provided for informational and educational purposes only and does not constitute investment advice, legal advice, tax advice, or a recommendation to buy, sell, or hold any security, commodity, or financial instrument.

The analysis presented herein reflects an Optimal Trust (OT) framework–based interpretation of publicly available information as of the date of publication. It is intended to help financial advisors contextualize geopolitical and market developments and support informed client conversations. It does not represent a prediction, guarantee, or definitive assessment of future events or market performance.

All market scenarios, probability-weighted outcomes, sector impacts, and trust scores are illustrative, not forecasts. Actual outcomes may differ materially due to changes in political decisions, legal rulings, regulatory actions, military developments, market conditions, or other unforeseen factors.

This content should not be relied upon as a primary basis for investment decisions. Financial advisors should conduct their own independent analysis, consider client-specific objectives, risk tolerance, and circumstances, and consult appropriate compliance, legal, or investment professionals before making any recommendations or portfolio adjustments.

References to specific countries, leaders, companies, sectors, or markets are made solely for analytical purposes and do not imply endorsement, condemnation, or factual certainty beyond what is reported by cited public sources. Information derived from news reporting is subject to revision as events evolve.

Neither Optimal Trust, TrustQ, nor the authors or contributors assume any responsibility for errors, omissions, or subsequent developments, nor for any losses or damages arising from the use of this material.

Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.

T Terms of Use Disclaimer Privacy Policy Contact Us

For more info call: (347)-474-8090

Copyright 2025, All Rights Reserved

© Copyright OPTIMAL TRUST